On March 11, 2021, President Joe Biden signed the American Rescue Plan Act of 2021 (the American Rescue Plan). Not only does the American Rescue Plan offer various incentive benefits due to the ongoing novel coronavirus pandemic (COVID-19) in 2019, it also expands the legitimate reasons for employee vacation and tax credits employers for providing paid vacation to employees under of the Families First Coronavirus Answer Act (FFCRA). In particular, the American rescue plan does not require employers to grant paid vacation. Vacation regulations under the requirements of the FFCRA are strictly voluntary with tax credits when vacation is granted.

FFCRA REFRESHER

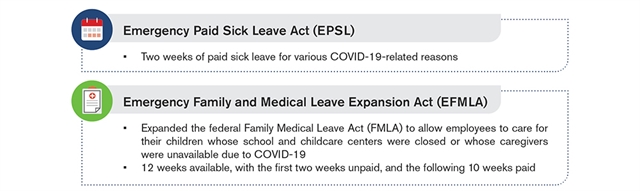

As a reminder, the FFCRA first came into force on April 1, 2020 and comprised two paid leave mandates for employers with fewer than 500 employees:

THE AMERICAN RESCUE PLAN

Shortly before the FFCRA expired on December 31, 2020, President Donald Trump signed the Consolidated Appropriations Act of 2021, which allows employers to continue offering the FFCRA vacation in exchange for a tax credit for qualified wages paid to employees until March 31, 2021.

The American Rescue Plan also does not require employers to grant paid vacation, but extends the previous tax credit from March 31, 2021 to September 30, 2021. In contrast to the Consolidated Appropriations Act, the American Rescue Plan also expands the legitimate reasons for Holidays under the EPSL and EFMLA and the amount of tax credits available.

Based on how the US Department of Labor (DOL) has responded to the publication of revisions to the FFCRA in the past, the DOL is likely to publish clarifying guidance in the form of a Frequently Asked Questions (FAQ) document in the near future. By then, it is important for employers to understand the impact of the US bailout plan on EPSL, EFMLA, and non-discrimination regulations.

Emergency paid sick leave

The American Rescue Plan expands the qualifying grounds for EPSL and resets the EPSL balance that employers can voluntarily provide to eligible employees to two weeks from April 1, 2021. In other words, if an employee has exhausted the original two weeks before April 1, 2021, employers have the option to provide that employee with an additional two weeks of EPSL between April 1, 2021 and September 30, 2021.

In particular, employees who have not exhausted the original two weeks of EPSL by April 1, 2021 will not transfer such vacation. For example, an employee who used one week of EPSL in 2020 will not have three weeks of ESPL after April 1, 2021.

The qualifying reasons for using EPSL include the six original reasons and three new reasons. The tax credit available to employers for paid vacation is based on the reason for the employee’s vacation, as set out below.

Law on Extension of Family Leave and Medical Leave

The American Rescue Plan expands the qualification reasons for EFMLA to include the original EFMLA qualification reasons (e.g., taking care of a child due to a school closure) and all of the above EPSL qualification reasons. In addition, the provision that the first two weeks of the EFMLA are not paid is deleted. As a result, employers can now voluntarily grant EFMLA paid leave of up to 12 weeks for a tax credit.

This means that employees who may have previously exhausted their 10-week EFMLA entitlement may be granted an additional two weeks of vacation at the discretion of their employer.

As a reminder, while the legitimate reasons for EPSL and EFMLA vacation are now similar, when an employee is provided EPSL, this is a separate benefit and does not reduce the amount of vacation granted under EFMLA. Accordingly, if an employer extends EPSL and EFMLA benefits after April 1, 2021, an employee may take up to 14 weeks of paid vacation and the employer will receive the appropriate tax credit.

Non-discrimination provisions

Finally, the American rescue plan warns that employers must not discriminate against highly paid employees, full-time employees, or employees based on their tenure when deciding on whether to grant leave. Failure to meet these requirements will result in ineligible tax credits.