IRS Points Steerage on Federally Funded COBRA Premium Subsidy: FAQs and What You Must Know

On March 25 and April 15, we reported on the 100% federally funded COBRA premium subsidy included in the American Rescue Plan Act (ARPA), summarizing Department of Labor (DOL) guidance and model notices, but noting the need for additional guidance on a number of issues. See “COVID-19 Resource Guide for Human Resources Professionals: 100% Federally Funded COBRA is Almost Here — What You Need to Know” and “DOL Issues Guidance on Federally Funded COBRA Premium Subsidy – FAQs and Model Notices Provide Clarification for Employers.” On May 18, the Internal Revenue Service (IRS) issued Notice 2021-31, providing much needed guidance on implementation and administration of the COBRA premium subsidy and refundable premium assistance tax credit in the form of 86 FAQs.

The ARPA COBRA premium subsidy provisions require employers and insurers to treat “assistance eligible individuals” (AEIs) as having paid 100% of the premiums otherwise owed for COBRA coverage (COBRA Subsidy) during the period from April 1, 2021 through September 30, 2021 (Subsidy Period). An AEI is a qualified beneficiary whose COBRA qualifying event is an involuntary termination of employment or reduction of hours, who is not otherwise eligible for Medicare or other group health plan coverage, and who actually elects COBRA coverage. The 86 FAQs are organized under several topics and cover a number of technical issues. This alert highlights several major issues that impact employers. Special rules apply for multiemployer plans or insured plans that are subject to state laws and employers subject to state mini-COBRA laws, which are outside the scope of this alert.

Eligibility for COBRA Subsidy

Loss of coverage due to a reduction in hours includes furloughs, lawful work stoppages, and voluntary reduction in hours. As a result of the COVID-19 pandemic, many employers implemented voluntary or involuntary furloughs/layoffs of employees. Some employees temporarily reduced their hours due to lack of daycare, school closings, or health problems. So long as there was a reasonable expectation to maintain the employment relationship and return to employment, the loss of coverage due to a temporary furlough or voluntary or involuntary reduction in hours, including lawful work stoppages, will qualify as a “reduction in hours” for purposes of determining potential AEI status.

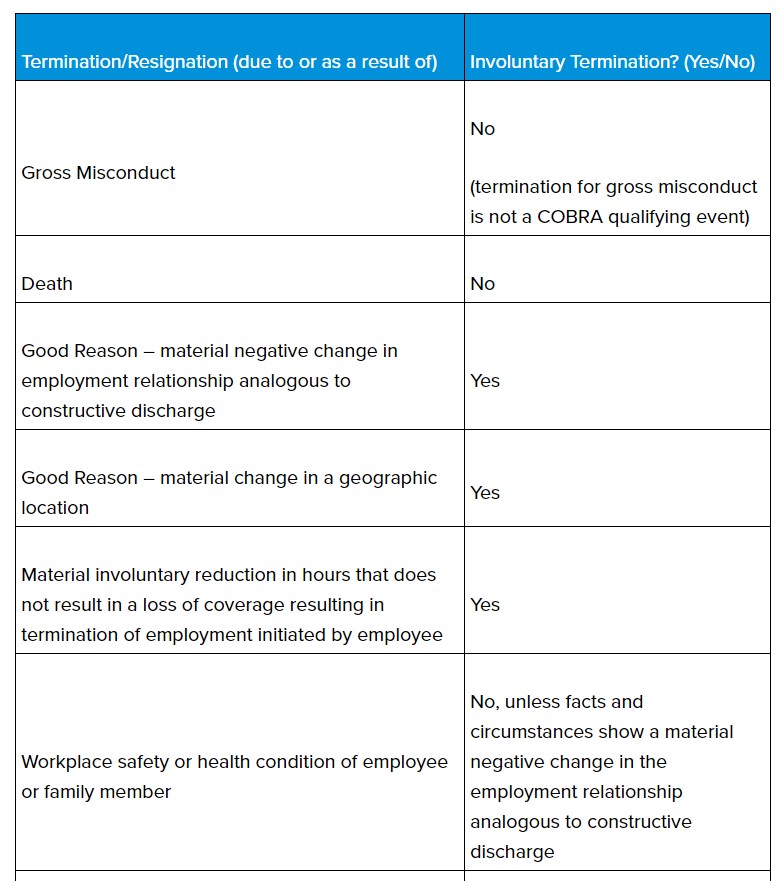

Involuntary termination includes termination for good reason and constructive discharge. For purposes of determining potential AEI status, a termination of employment is “involuntary” if, based on the facts and circumstances, the termination is due to independent exercise of unilateral authority of the employer to terminate employment other than due to an employee’s implicit or explicit request, where the employee was willing and able to continue performing services. A resignation or voluntary termination may qualify as an “involuntary” termination if, based on the facts and circumstances, the termination was analogous to constructive discharge. The following chart provides examples of terminations that qualify (and do not qualify) as an involuntary termination for purposes of AEI status:

COBRA ElectionAn individual may become a potential AEI more than once. For example, on April 1, 2021, an individual’s employment is involuntarily terminated, he becomes a qualified beneficiary and elects COBRA; therefore, he becomes an AEI on April 1. On July 1, 2021, the individual becomes eligible for coverage under a group health plan (GHP) sponsored by the employer of the individual’s spouse at which time the individual ceases to be an AEI. The individual enrolls in the GHP sponsored by the spouse’s employer. On August 1, 2021, the individual’s spouse has an involuntary termination of employment resulting in loss of coverage. The spouse and individual elect COBRA continuation under the GHP maintained by the spouse’s employer and therefore become AEIs as of August 1, 2021.

AEI determination is made at the time of the first qualifying event. A reduction in hours or involuntary termination of employment that follows an earlier qualifying event, such as a divorce, does not make the qualified beneficiary from the first qualifying event a potential AEI.

An AEI must inform the employer if the individual ceases to be an AEI during the Subsidy Period. An individual ceases to be an AEI if he becomes eligible for other group health plan coverage or Medicare. An individual who fails to notify the employer of his ineligibility will be subject to a federal tax penalty of $250 (or, in the case of a fraudulent failure to notify, the greater of $250 or 110% of the COBRA Subsidy improperly received), unless the failure was due to reasonable cause and not willful neglect.

Employers may require and rely on individuals’ self-certification or attestation of their COBRA Subsidy eligibility, unless the employer has actual knowledge of ineligibility. The IRS clarified that an employer can rely on the individual’s attestation of eligibility for the COBRA Subsidy, including the fact that the individual is not eligible for disqualifying coverage (e., other GHP coverage or Medicare). It may not be readily apparent to the individual administering the GHP if a termination of employment is voluntary or involuntary. For example, it is not unusual for an employer and employee to call an involuntary termination of employment a retirement or voluntary termination as part of a settlement agreement or for an employee to resign preemptively to avoid being fired. An individual’s self-certification or attestation that the loss of coverage was due to an involuntary termination or reduction in hours (given the facts and circumstances) is helpful for these types of circumstances. The DOL provided a model form attestation that can be used for this purpose. See “Request for Treatment as an Assistance Eligible Individual” Request for Treatment as an Assistance Eligible Individual” form.

Coverage eligible for the COBRA Subsidy includes GHPs (medical, dental-only, and vision-only plans), HRAs, and retiree coverage, but only if the retiree coverage is offered under the same GHP as coverage available for similarly situated active employees. The FAQs provide special rules for HRAs. The COBRA Subsidy is unavailable for plans not subject to federal COBRA or state mini-COBRA (g., group term life, health FSAs, qualified small employer HRAs, Medicare, and church plans). Also, the COBRA Subsidy is unavailable for coverage with premiums greater than the premium for coverage in which the individual was enrolled at the time of the qualifying event, unless such plan is no longer available.

The COBRA Subsidy applies to months during an extended COBRA period that overlaps with the COBRA Subsidy Period. The COBRA Subsidy is available to individuals who have elected and remained on COBRA continuation coverage for an extended period due to a disability determination, second qualifying event, or an extension under state mini-COBRA, to the extent those additional periods of coverage include months that fall between April 1, 2021 and September 30, 2021, if the original qualifying event was a reduction in hours or an involuntary termination of employment.

COBRA Subsidy beginning date and ending date. The COBRA Subsidy begins on the date premiums would normally be charged and ends on the earlier of (i) eligibility for other GHP or Medicare coverage, (ii) cessation of eligibility for COBRA, or (iii) the end of the last period of coverage beginning on or before September 30, 2021. For example, for bi-weekly premiums, the final coverage period of September 19 through October 2, 2021 would be eligible for COBRA Subsidy, even for the two days in October that fall after September 30, 2021. Death of the employee during the COBRA Subsidy Period does not end other qualified beneficiary, spouse, or dependent children coverage or subsidy eligibility. Any COBRA continuation coverage extending beyond the end of the COBRA Subsidy Period continues unsubsidized.

Extended COBRA election periods apply for qualified beneficiaries without elections in effect on April 1, 2021 but would otherwise have been an AEI. A qualified beneficiary whose qualifying event was a reduction in hours or an involuntary termination of employment is a potential AEI and must be offered the ARPA extended election period for any health coverage the qualified beneficiary was enrolled in prior to the qualifying event and for which the individual does not have a COBRA election in effect on April 1, 2021, even if the qualified beneficiary previously elected COBRA continuation coverage for other coverage in which the qualified beneficiary was previously enrolled. For example, a spouse or dependent child who is a beneficiary under a GHP on the day before the employee’s reduction in hours or involuntary termination that resulted in loss of coverage also would be potential AEIs. If the employee elected self-only coverage, the spouse or dependent child in this situation has a second election opportunity. As another example, suppose a qualified beneficiary who lost coverage due to a reduction in hours or involuntary termination of employment was offered COBRA for health, dental-only, and vision-only coverage but only elected COBRA continuation coverage for the dental-only and vision-only coverage. This individual must be offered the extended election period for the health coverage for which he was enrolled prior to the qualifying event. If the individual elects retroactive COBRA coverage under the original COBRA election period (prior to the ARPA extended election period), the COBRA coverage is retroactive to that individual’s loss of active coverage, but the COBRA Subsidy does not apply for periods of coverage prior to the first period of coverage beginning on or after April 1, 2021.

Premium Assistance Credit

IRS FAQs detail technical requirements for premium payees (common-law employer maintaining the plan, multiemployer plan, and insurers for insured plans subject to state laws) to determine eligibility for, and the amount of, the premium assistance credit (Credit) and the mechanics of reporting and requesting the Credit. Following are key points applicable for common-law employers subject to federal COBRA. Additional details regarding multiemployer plans, third-party payees/professional service organizations, and small employer plans subject to state mini-COBRA laws are beyond the scope of this alert, so employers impacted by those rules should refer to the FAQs and consult benefits counsel.

Employers claiming the Credit must retain records substantiating the individual’s eligibility for the COBRA Subsidy. The employer can rely on an individual’s attestation of eligibility or maintain other documentation of eligibility until the individual notifies the employer that he ceases to be an AEI, unless the employer has actual knowledge that the individual is ineligible. The DOL model form attestation can be used for this purpose. See “Request for Treatment as an Assistance Eligible Individual” Request for Treatment as an Assistance Eligible Individual” form.

The employer can request the Credit as of the date it receives the potential AEIs COBRA election for any periods of coverage that began prior to such date and thereafter as of the beginning of each period of coverage. If the employer learns that the AEI is no longer eligible for the COBRA Subsidy (g., due to eligibility for other coverage), the employer is not entitled to the Credit from that point forward.

The employer cannot claim a Credit with for amounts considered as qualified wages or qualified health plan expenses. The Employee Retention Tax Credit, which allows a payroll tax credit for certain qualified wages, was extended to include qualified wages up to $28,000 per employee paid through December 31, 2021. Likewise, the payroll credit under the Families First Coronavirus Response Act for emergency paid sick leave and emergency family and medical leave was extended to cover qualified family leave wages through September 30, 2021. The employer cannot double dip.

The employer claims the Credit for a quarter on its federal employment tax return (usually Form 941). The employer may reduce the deposits of federal employment taxes, including withheld taxes, that it would otherwise be required to deposit, up to the amount of the anticipated Credit and request an advance of the anticipated Credit that exceeds the federal employment tax deposits available for reduction by filing Form 7200.

The Credit for a quarter is equal to premiums not paid by AEIs. The amount not paid by AEIs is the premium amount charged for COBRA coverage to other similarly situated covered employees and qualified beneficiaries, including any administrative costs (generally 102%). For an individual coverage HRA, the amount is limited to 102% of the actual amount reimbursed to the AEI. The Credit does not apply for any qualified beneficiaries who are not AEIs. For example, an AEI has self-only coverage that would cost $450 per month absent the COBRA Subsidy. During the extended election period, the plan has open enrollment and allows active employees and qualified beneficiaries to add spouses and dependents. The AEI adds a spouse and one dependent child who were not covered before the employee’s qualifying event. The COBRA premiums absent the COBRA Subsidy are $1,100 per month. The Credit is limited to $450 per month. If the total cost of the coverage for all covered individuals does not exceed the premium costs for the AEIs alone, then the premium for the individual who is not an AEI is zero, and the COBRA Subsidy is the full applicable COBRA premium.

The Credit is reduced to the extent the employer subsidizes COBRA premium costs for similarly situated qualified beneficiaries who are not AEIs. For example, an employer with a severance plan subsidizes $600 of the $1,000 per month COBRA premium. In this case, the Credit is limited to $400 per month — the amount paid by similarly situated employees. Here, the employer can increase the maximum premium allowed under COBRA for all similarly situated employees or tax the subsidized portion to the employee to increase the Credit. A plan amendment and notices may be required to take these proactive measures to increase a reduced Credit. Employers should consult with benefits counsel prior to taking any such proactive measures. See FAQs 64 through 66 for other examples of these limitations.